The TheraRadar Brief

Every drug has multiple stories. Most never get told.

IGF-1R: 20 Years of Cancer Failures, Then a $2 Billion Eye Drug

Pfizer, Amgen, Lilly, Merck, and Astellas all failed at IGF-1R in cancer. Then a shelved Roche antibody became the only effective treatment for thyroid eye disease. Same receptor, completely different biology.

Get the next TheraRadar Brief in your inbox

Drug development, biology, and market dynamics — free, every week.

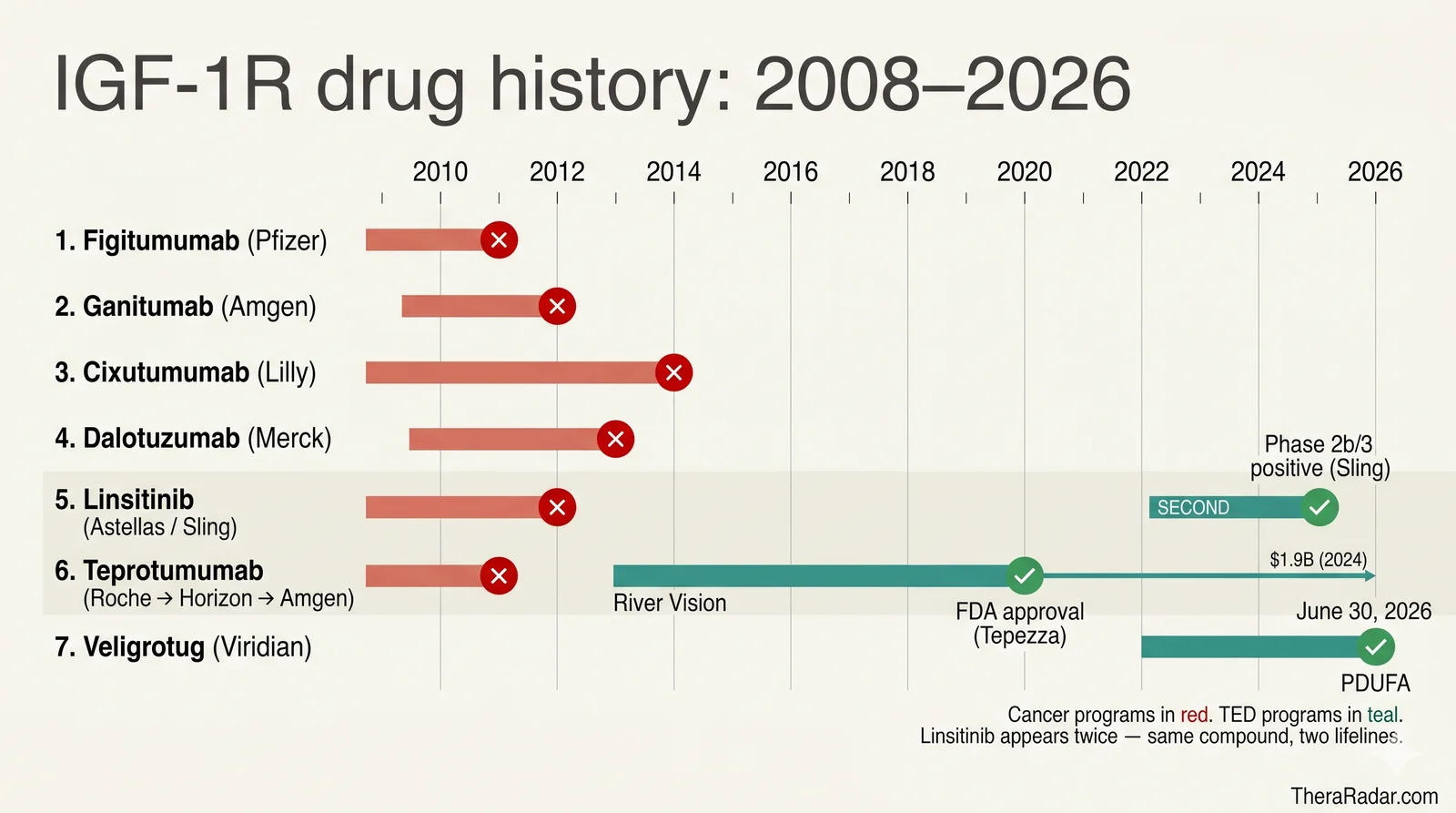

Five companies bet on IGF-1R in cancer between 2005 and 2015 — Pfizer, Amgen, Lilly (via ImClone), Merck, and Astellas/OSI. Every Phase 3 trial failed. Cumulative oncology approvals: zero.

The only IGF-1R drug that ever made it to FDA approval treats none of those cancers. Teprotumumab — Tepezza — was approved for thyroid eye disease and generated $1.9 billion in 2024. Horizon, the company that acquired the program, originally projected peak sales of just over $250 million. They under-forecast their own drug by nearly 8×.

Tepezza proved IGF-1R is not a bad target. But for 20 years, the cancer trials were testing it in the wrong disease.

The hypothesis that swept oncology

In the late 1990s, IGF-1R looked like the next great cancer target. The biology was clean. IGF-1R is the receptor for insulin-like growth factor 1, a hormone that drives cell proliferation and survival via the PI3K/AKT and MAPK pathways. Mouse studies showed that animals lacking IGF-1R were strikingly resistant to tumor formation. Tumor samples showed IGF-1R overexpression across breast, prostate, lung, colon, and sarcoma. Cell-line experiments showed that blocking the receptor slowed growth and triggered apoptosis.

IGF-1R also looked like a resistance escape route for two of pharma's biggest hits. Cells treated with EGFR inhibitors (Iressa, Tarceva) or HER2 inhibitors (Herceptin) often upregulated IGF-1R as a compensatory survival route. Block IGF-1R, the thinking went, and you'd both kill cancer directly and re-sensitize tumors to existing drugs. Every major pharma had a program by 2008.

The IGF-1R Cancer Drug Graveyard

Pfizer — figitumumab (CP-751,871). Two Phase 3 trials in non-small-cell lung cancer. ADVIGO 1016 combined figitumumab with paclitaxel/carboplatin in first-line; the Data Safety Monitoring Committee halted enrollment in September 2009 after observing more serious adverse events — including fatalities — in the treatment arm. ADVIGO 1018 combined figitumumab with erlotinib in previously-treated patients; also discontinued for futility. Pfizer ceased development entirely in January 2011.

Amgen — ganitumab (AMG 479). Phase 3 GAMMA trial in metastatic pancreatic cancer combined ganitumab with gemcitabine. Among 800 randomized patients, median overall survival was 7.0–7.2 months across both ganitumab dose arms versus 7.2 months for placebo + gemcitabine — no benefit at all. Trial terminated August 8, 2012. Amgen later tested ganitumab in Ewing sarcoma — also negative. Program ended.

ImClone / Eli Lilly — cixutumumab (IMC-A12). Lilly inherited the program when it acquired ImClone. Cixutumumab ran through more than 45 Phase 1 and Phase 2 trials in NSCLC, sarcoma, breast, prostate, pancreatic, hepatocellular, and ocular melanoma — almost the full solid-tumor catalog. None showed enough benefit to justify Phase 3. Lilly removed cixutumumab from its pipeline. The program never reached Phase 3 — it ran out of Phase 2 indications first.

Merck — dalotuzumab (MK-0646). Phase 2/3 trial in chemorefractory KRAS-wild-type metastatic colorectal cancer added dalotuzumab to cetuximab + irinotecan. The trial was discontinued early for futility, but the data showed something worse than negative — patients on dalotuzumab had shorter median progression-free survival (3.9–5.4 months across two dose arms vs 5.6 months for placebo + cetuximab + irinotecan) and shorter overall survival (10.8–11.6 months vs 14.0 months for placebo). Adding the IGF-1R antibody to a working backbone actively harmed outcomes. Program discontinued.

Astellas / OSI Pharmaceuticals — linsitinib (OSI-906). A small-molecule dual IGF-1R/insulin receptor inhibitor. Phase 3 in adrenocortical carcinoma — a small but desperate-need indication — failed both primary endpoints. The trial was unblinded March 19, 2012 by recommendation of the Data Monitoring Committee. Median OS was 323 days for linsitinib versus 356 days for placebo (hazard ratio 0.94, p=0.77). Lancet Oncology published the full results in 2015.

Roche / Genmab — teprotumumab (RG1507). Genmab developed the anti-IGF-1R antibody and licensed it to Roche for cancer development. Tested in NSCLC and Ewing sarcoma with only modest efficacy. Roche discontinued the program in December 2009.

Six programs, five Phase 3 failures, zero approvals.

Why it didn't work

The post-mortems converged on three reasons.

1. Insulin receptor crosstalk. IGF-1R and the insulin receptor (IR) are structurally near-identical. Both are receptor tyrosine kinases with the same architecture — two extracellular α-subunits that bind ligand, two transmembrane β-subunits that carry the kinase — and their kinase domains share ~84% sequence homology. In tissues expressing both, they form hybrid receptors with one IR half and one IGF-1R half. Insulin binds IR with high affinity and drives glucose uptake; IGF-1 binds IGF-1R and drives mitogenic, anti-apoptotic signaling; each hormone also binds the other receptor with lower affinity. Most IGF-1R antibodies and small molecules partially blocked insulin signaling too, and patients developed hyperglycemia, sometimes severe.

2. Compensatory upregulation. When IGF-1R was blocked, cancer cells frequently upregulated the insulin receptor itself, which can also signal through PI3K/AKT and drive proliferation. Tumor growth routed around the block and resumed.

3. The receptor wasn't a bottleneck. Cancer cells have many overlapping pro-survival and proliferation pathways: EGFR, HER2, MET, FGFR, VEGFR, the PI3K/AKT axis itself, RAS/RAF/MEK/ERK. IGF-1R contributed to growth but was rarely the required node. Combination trials with stronger backbones (gemcitabine, erlotinib, cetuximab) failed because IGF-1R's contribution was too small to add measurable benefit on top.

Plus the patient selection problem. Unlike HER2 (where IHC and FISH define the target population) or BRCA (where genetic testing identifies the responders), no one ever found a clinical biomarker that selected "IGF-1R-driven" tumors. Trials enrolled unselected patients and accepted the dilution. By 2015, the field was effectively dead.

How Teprotumumab Was Salvaged and Became Tepezza

While oncology had been treating IGF-1R as a growth-receptor target, an entirely different conversation had been happening in endocrinology.

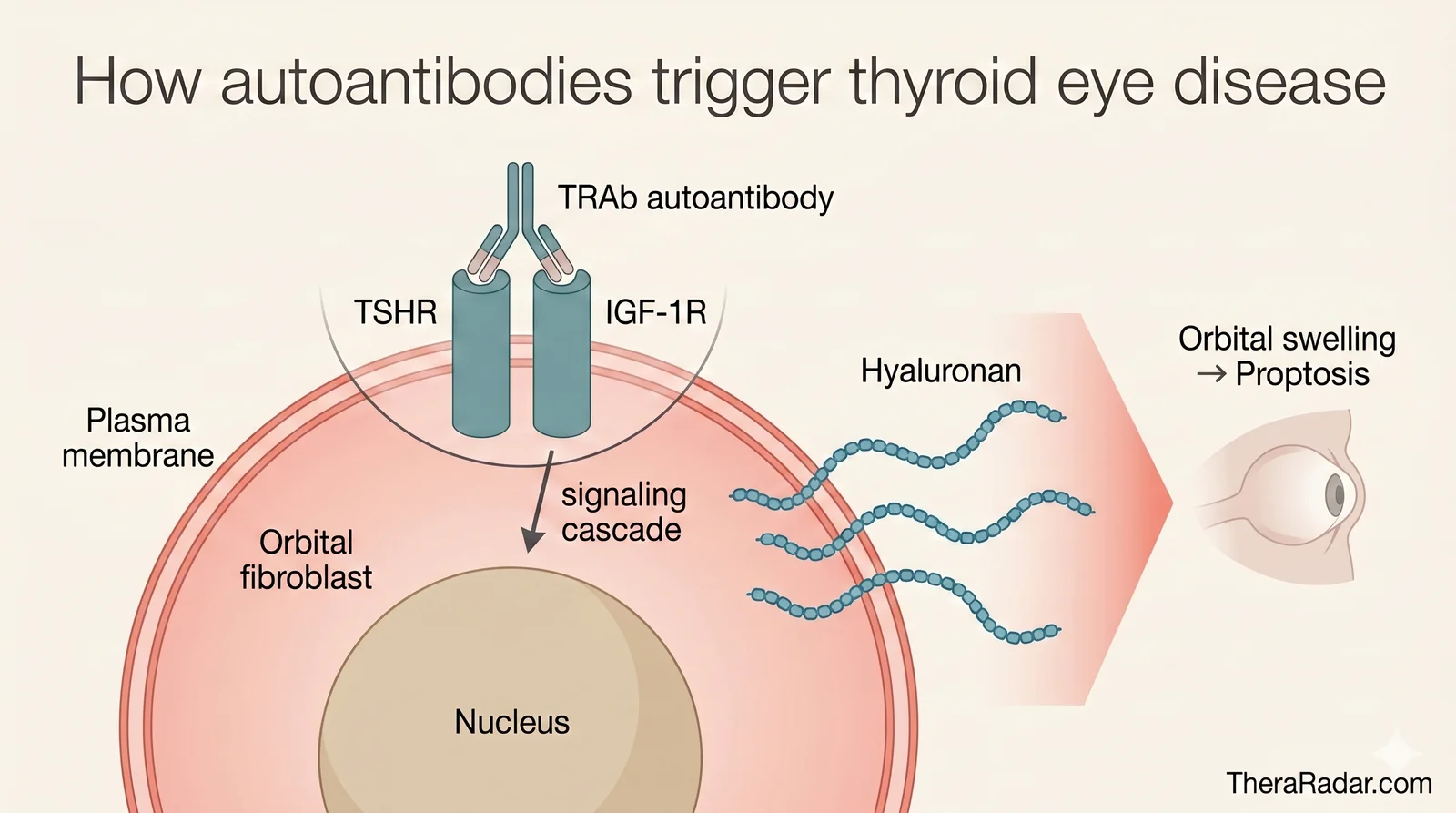

Starting around 2003, Dr. Terry Smith — then at Harbor-UCLA Medical Center, later at the University of Michigan — and collaborators including Pritchard, Cruikshank, and Hoa published a series of papers showing that orbital fibroblasts (the connective-tissue cells behind the eye) expressed IGF-1R unusually highly, and that Graves' disease immunoglobulins acted through the IGF-1R pathway to drive fibroblast inflammation. Later work confirmed that IGF-1R physically associated with the TSH receptor (TSHR) on those cells; pull-down studies brought both proteins out of solution from a single antibody, and confocal microscopy showed the two receptors co-localized — they function as a complex on orbital fibroblasts (Tsui et al., J Immunol 2008). Critically, IgG from Graves' patients drove hyaluronic-acid production in orbital fibroblasts, and an IGF-1R-blocking monoclonal antibody shut that production down. Smith's hypothesis: in thyroid eye disease, IGF-1R isn't acting as a growth receptor at all — it's engaged by autoantibodies that bind the TSHR/IGF-1R complex and activate an autoimmune cascade.

If Smith was right, blocking IGF-1R in TED would work because the receptor sits on a required node of the autoantibody circuit — not because it drives growth. The receptor doesn't have to be the dominant driver of any biology; it just has to be necessary for the autoimmune loop.

A startup called River Vision Development, founded by Narrow River Management LP for the sole purpose of developing teprotumumab, in-licensed the shelved antibody from Roche/Genmab. River Vision had Smith on its scientific advisory board and was built around the TED hypothesis. Their Phase 2b trial produced what the cancer trials never had: replicable response. Proptosis (eye bulging) reduced by millimeters; diplopia (double vision) resolved.

On May 8, 2017, Horizon Pharma announced the acquisition of River Vision for $145 million upfront ($151.9M total cash including cash acquired) plus contingent milestone and earn-out payments. At the time, Horizon publicly projected peak annual U.S. net sales for teprotumumab — if approved — at over $250 million. Horizon ran the Phase 3 OPTIC trial. Tepezza was approved by FDA in January 2020. By 2024, the drug was generating $1.9 billion annually — roughly 8× Horizon's own peak forecast at the time of acquisition.

(Amgen acquired Horizon in October 2023 for $27.8 billion, with Tepezza as the centerpiece asset.)

What thyroid eye disease actually is

Thyroid eye disease (TED) is an autoimmune attack on the orbital tissues — the fat, connective tissue, and muscles behind the eye. It typically appears in patients with Graves' disease, the autoimmune cause of hyperthyroidism, and shares the same autoantibody biology.

Those autoantibodies are TSH receptor antibodies (TRAb, also known as thyroid-stimulating immunoglobulins). In Graves' patients, B cells mistakenly produce antibodies against the body's own TSH receptor — the receptor that normally signals thyroid cells to produce thyroid hormone. The antibodies act as constitutive fake TSH signals: they latch onto TSH receptors and drive the thyroid into chronic overproduction (the hyperthyroidism that defines Graves'). In the orbit, the same antibodies bind the TSHR/IGF-1R complex on fibroblasts and activate the IGF-1R signaling Smith's group identified.

The downstream result is physical remodeling of the orbit. Hyaluronan pours into the orbital fat and expands it. The extraocular muscles thicken. The eyeball gets pushed forward (proptosis), the eyelids retract, and the swollen muscles can no longer coordinate eye movement, producing double vision (diplopia). In severe cases the inflated tissue compresses the optic nerve and threatens sight.

The active inflammatory phase lasts roughly 6 to 18 months before stabilizing into a fibrotic "burnt-out" phase. About 100,000 Americans have TED.

Before Tepezza, the only options were corticosteroids (broad immunosuppression with significant side effects), orbital radiation, and surgical decompression of orbital fat and bone. None reliably reversed proptosis.

Want the next brief? Subscribe — free, every week.

The biological twist

The cancer programs and Tepezza were hitting the same receptor in completely different roles.

In cancer, IGF-1R is one of many growth signals. Blocking it slows but doesn't stop proliferation; tumors route around the block.

In TED, IGF-1R is engaged by autoantibodies as part of a TSHR-coupled complex on orbital fibroblasts. Blocking it breaks the autoimmune loop — inflammation reverses, hyaluronan deposition stops, and orbital tissue remodels back toward normal.

Target-driven drug discovery often confuses the two situations. A validated target tells you the receptor is wired into a relevant pathway. It doesn't tell you whether that pathway dominates the disease you're chasing. The same molecule can be a peripheral contributor in one condition and a required node in another.

What it cost — and what it saved

Figitumumab and ganitumab alone enrolled close to 2,000 Phase 3 patients between them, with thousands more in the Phase 2 programs across the six companies. The cancer-IGF-1R era ran for roughly a decade and produced zero approvals.

Tepezza, the surviving program, generated $1.9 billion in 2024 revenue ($460M in Q4 2024 alone) for Amgen, and grew another 29% year-over-year to $490M in Q1 2026. Amgen reported more than 25,000 U.S. patients treated since launch — still a small fraction of the ~100,000 estimated U.S. TED patient population.

Amgen-reported net product sales. Bars scaled to the Q3 2025 peak of $560M. The Q1 2025 dip was an inventory destocking quarter, not a real demand drop.

Annual totals: 2024 = $1.85B, 2025 = $1.90B (essentially flat YoY). The Q1 2026 number was reported by Amgen on April 30, 2026; the 29% YoY growth cited at the top of the section reflects Q1 2026 vs the soft Q1 2025 compare. Source: Amgen 10-K filings and Q1 2026 press release; data file at data/amgen-revenues.json.

Then a second drug worked. And a third, and a fourth.

Five years after Tepezza's approval, at least eleven IGF-1R-targeted programs are in clinical trials for thyroid eye disease, spanning Phase 1 through FDA review.

Viridian Therapeutics' veligrotug (VRDN-001) is the most advanced challenger — an IV monoclonal antibody targeting IGF-1R, like teprotumumab. Phase 3 THRIVE and THRIVE-2 trials reported positive topline data with comparable proptosis-response rates and a lower observed rate of hearing-related adverse events than Tepezza's labeled rate. The FDA accepted the BLA with a PDUFA target action date of June 30, 2026. Whichever way that decision lands, the Phase 3 data already validate the underlying mechanism.

Viridian's VRDN-003 is a subcutaneous IGF-1R antibody in Phase 3, designed for at-home dosing rather than IV infusion. Zai Lab licensed VRDN-003 for Greater China as ZL-1109, also in Phase 3.

Beyond Viridian, three other developments matter on the FDA side:

- Sling Therapeutics already resurrected linsitinib for TED. Sling launched in June 2022 with a $35M Series A from TPG's The Rise Fund, in-licensing from Astellas the same oral small molecule (OSI-906) that had been terminated in adrenocortical carcinoma a decade earlier. The Phase 2b/3 LIDS trial reported positive topline data in January 2025, meeting its primary endpoint of proptosis reduction at the 150mg BID dose. A confirmatory Phase 3 is now underway. Same compound. Same dosing. Different disease — and it worked. The drug that failed in cancer because IGF-1R wasn't the bottleneck there is now an oral TED therapy in late-stage development.

- Amgen is double-hedging Tepezza. In Phase 1/2 it has AMG 732, an entirely new IGF-1R molecule. And in April 2026 Amgen reported positive Phase 3 data for a subcutaneous on-body-injector formulation of Tepezza itself — same teprotumumab molecule, easier delivery (77% proptosis response at week 24 vs 19.6% for placebo). The company that paid $27.8 billion for Tepezza is racing to defend both the molecule and the route of administration before Viridian's subQ VRDN-003 reaches the market.

- Acelyrin's lonigutamab has cleared Phase 1/2; Lassen Therapeutics' LASN01 has completed multiple Phase 1/2 studies.

Outside the FDA process, multiple Chinese pharmas — Innovent (IBI311), Minghui (MHB018A), Nanjing Chia-tai Tianqing (NTB003), and GeneScience (GenSci098) — are running their own IGF-1R-for-TED programs aimed at the NMPA. The China pipeline doesn't intersect the U.S. competitive picture but adds independent confirmation that the hypothesis travels.

Non-IGF-1R mechanisms have also been tried in TED, with mixed results. Roche's satralizumab (IL-6R) is in Phase 3. Tocilizumab (IL-6R) showed positive academic-trial signals. Batoclimab (FcRn antagonist, Immunovant) ran Phase 3. Novartis's secukinumab (IL-17A) Phase 3 in TED was terminated. The lesson holds inside TED itself: even within a single autoimmune indication, only certain mechanisms work — and IGF-1R is the standout.

With eleven mechanistically-related drugs converging on the same disease — including the exact compound that failed in cancer — Tepezza is no longer the only proof of Smith's hypothesis. The 20-year cancer graveyard seeded a global franchise that Amgen is now racing to extend before competitors arrive.

The pattern

IGF-1R isn't unique. The same shape shows up across pharma history:

- mTOR — Everolimus (Afinitor) failed in many oncology indications before finding niche approvals; rapamycin's most enduring use is now in transplantation immunosuppression and a small subset of cancers.

- NF-κB inhibitors — pursued aggressively for cancer in the 2000s, mostly failed; the surviving compounds are useful in inflammation.

- Chk1 inhibitors — repeatedly failed in cancer; renewed interest in DNA-damage contexts that don't look like the original hypothesis.

Drugging a receptor depends on what activates it and which circuits depend on it. IGF-1R was a marginal contributor to cancer growth. It was a required node in TED's autoantibody loop. That difference is what determined whether the target was druggable.

For IGF-1R, the disease where it was the bottleneck happened to be thyroid eye disease. Oncology spent two decades asking the wrong question.

Go deeper with Pro

Pro gives you the data — patent cliffs, trial analytics, competitive landscapes, revenue tracking. Briefs tell the story with the data. Launch pricing: $99/month.

See Pro plansGet the next Brief in your inbox — free

Every drug has multiple stories. Most never get told. One brief every week. No spam.

Archive at /briefs/. Unsubscribe anytime.

Sources

- Figitumumab Phase 3 termination: Pfizer Discontinues Phase 3 Trial of Figitumumab in NSCLC for Futility — Pfizer (2009)

- Ganitumab GAMMA trial: Fuchs et al., GAMMA Phase 3 of ganitumab + gemcitabine in pancreatic cancer — Cancer (2015)

- Cixutumumab program history: Cixutumumab clinical-trial summary (Wikipedia)

- Dalotuzumab Phase 2/3 mCRC: Sclafani et al., Randomized Phase 2/3 of Dalotuzumab in KRAS-wt mCRC — J Clin Oncol (2015)

- Linsitinib in adrenocortical carcinoma: Fassnacht et al., Linsitinib vs placebo Phase 3 — Lancet Oncology (2015)

- Roche discontinues RG1507: Genmab Announces Roche to Discontinue RG1507 — December 2009

- Graves' IgG → IGF-1R pathway: Pritchard et al., Immunoglobulin Activation of T Cell Chemoattractant via IGF-1R — J Immunol (2003)

- TSHR/IGF-1R physical association: Tsui et al., Evidence for an association between TSH and IGF-1 receptors — J Immunol (2008)

- Bidirectional TSH/IGF-1R cross-talk: Krieger et al., Bidirectional TSH and IGF-1 Receptor Cross Talk Mediates Hyaluronan Secretion — PMC (2015)

- IGF-1R / TED comprehensive review: Smith TJ, Insulin-like Growth Factor-I Receptor and Thyroid-Associated Ophthalmopathy — Endocrine Reviews (2019)

- Horizon acquires River Vision (Tepezza): Horizon Pharma to Acquire River Vision Development — May 2017

- Amgen acquires Horizon Therapeutics: Amgen Completes Acquisition of Horizon Therapeutics — October 2023

- Tepezza 2024 revenue ($1.9B): Amgen Q4 + Full Year 2024 Financial Results — February 2025

- Tepezza Q1 2026 revenue + patient counts: Amgen Q1 2026 Financial Results — April 2026

- Subcutaneous Tepezza Phase 3 positive: Amgen Announces Positive Topline Phase 3 for Subcutaneous Tepezza — April 2026

- Sling Therapeutics launch: Sling Therapeutics Launches with $35M Series A — June 2022

- Sling LIDS Phase 2b/3 positive topline: Sling LIDS Phase 2b/3 Topline Results — January 2025

Spot an error? Reach out at hello@theraradar.com.